When you’re looking for a generally safe, steady, and predictable way to grow your savings, Certificates of Deposit (CDs) can be a reliable financial tool. CDs typically offer higher interest rates than traditional savings accounts, guaranteed returns, and the security of FDIC insurance — making them an excellent option for both new savers and experienced investors.

At Utah Independent Bank (UIB), we provide CD options designed to help individuals, families, and businesses grow their money confidently. Whether you're saving for a future purchase, planning ahead for college, or simply building long-term wealth, understanding how CDs work can help you make smarter financial decisions.

This guide covers some things you need to know about CDs, how they benefit your financial plan, and how UIB’s CD rates and terms can help you make the most of your savings.

What Is a Certificate of Deposit (CD)?

A Certificate of Deposit is a type of fixed-term savings account that pays a guaranteed interest rate in exchange for keeping your money deposited for a set period of time. Unlike regular savings accounts, CDs reward you for committing your funds — typically offering higher interest rates and defined returns.

CD Basics

- Fixed term: Usually ranges from 3 months to 5 years

- Fixed interest rate: Locked in at the time you open the CD

- FDIC insured: Up to the federal limit for peace of mind

- Defined returns: Your principal and interest are protected

CDs are one of the safest ways to grow your money without market risk.

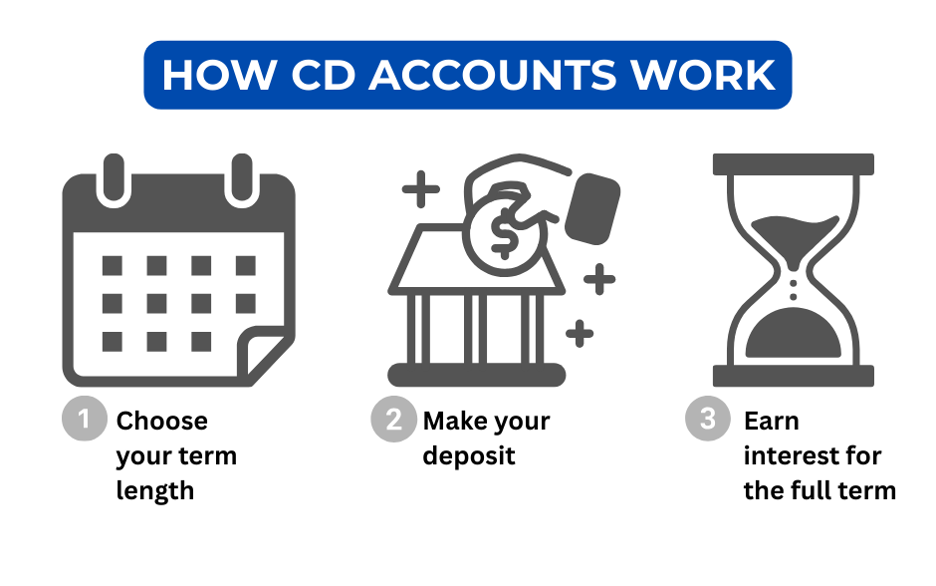

How Do CD Accounts Work?

Here’s the simple step-by-step process:

1. Choose your term length.

UIB offers a variety of CD terms with different interest rates.

2. Make your deposit.

You deposit a minimum amount (Please contact a UIB Branch for minimum deposit requirements).

3. Earn interest for the full term.

Your money grows at a set interest rate.

4. Withdraw at maturity.

When your CD reaches its end date (“matures”), you can withdraw your balance or renew it. (Terms and conditions apply)

Because the rate is fixed, you earn the same predictable return no matter what happens in the market — a major advantage for long-term planners and cautious savers.

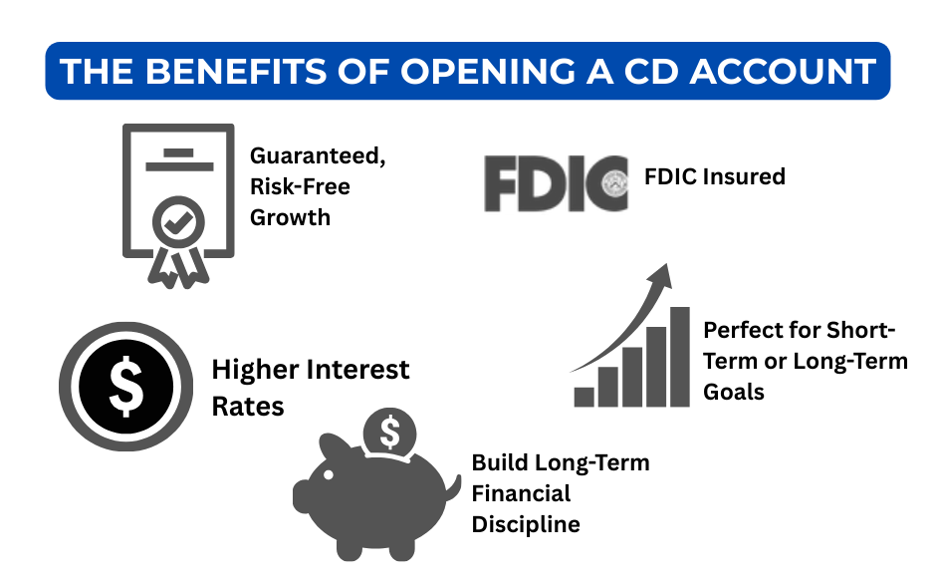

The Benefits of Opening a CD Account

CDs offer multiple advantages that make them ideal for financial planning at almost any stage of life.

1. Defined growth, with Minimal Risk

UIB CDs come with a fixed interest rate, meaning your earnings never fluctuate. This is perfect for anyone who prefers predictable returns over market volatility.

2. Higher Interest Rates Than Traditional Savings

Because you commit your money for a set time, banks reward you with higher yields. UIB CD rates are competitive and designed to give you more value for your savings.

3. FDIC Insured for Maximum Safety

Every UIB CD is FDIC insured up to the federal limit, (Please visit FDIC.gov for limitations) protecting your principal and interest. This makes CDs one of the safest investments available today.

4. Helps Build Long-Term Financial Discipline

Since withdrawing early may result in penalties, CDs can help reinforce healthy savings habits by keeping your money untouched until maturity.

5. Perfect for Short-Term or Long-Term Goals

- You can align CD terms with your goals, such as:

- A down payment on a home

- A future car purchase

- College or trade school tuition

- Vacation savings

- Emergency funds you want to grow safely

Understanding CD Terms and Rates

CDs vary in length and rate, so picking the right one matters.

Short-Term CDs (3–12 Months)

- Ideal for parking money you may need soon

- Earn more than a basic savings account

- Useful for seasonal or short-term goals

Medium-Term CDs (12–36 Months)

- Balance between higher earnings and flexibility

- Great for future purchases or planned expenses

Long-Term CDs (3–5 Years or More)

- Best for long-term savings or wealth-building strategies

UIB provides transparent and competitive CD rates tailored to Utah residents and businesses. Reviewing the current UIB CD rates helps you choose the best option for your financial goals.

How UIB’s CD Options Work

At Utah Independent Bank, we make the CD process simple, secure, and personalized. When you open a CD with UIB, you benefit from:

✔ Local Customer Service

Work with real people right here in Utah who understand your goals.

✔ Competitive Fixed Rates

Earn more on your savings with reliable return and limited risk.

✔ Flexible Terms

Choose from multiple term lengths based on your timeline.

✔ Low Minimum Deposits

CDs are accessible even if you’re just starting out.

✔ Automatic Renewal Options

Let your CD roll over automatically or adjust your strategy as your needs change.

Whether you're a first-time saver or someone with a full financial plan, UIB’s CD options offer flexibility and value.

Who Should Consider a CD Account?

CDs are ideal for:

✔ Conservative Savers

Those who prefer stable, predictable growth over investing in stocks.

✔ Goal-Based Savers

Perfect for major purchases or future savings goals.

✔ Retirees

A reliable way to earn fixed income with limited market exposure.

✔ Young Adults & Families

A smart start to long-term financial planning.

✔ Businesses

Companies can park excess cash in CDs to earn more while keeping funds secure.

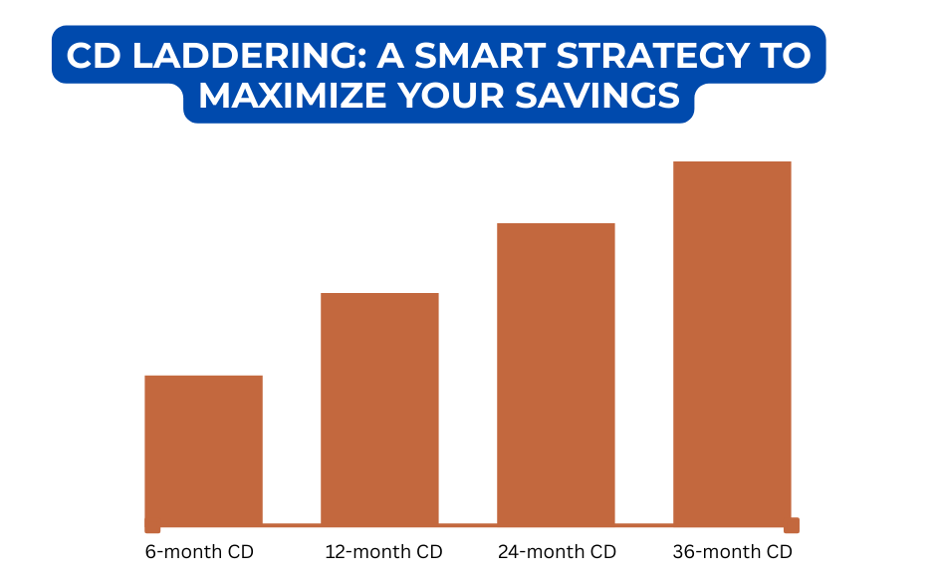

CD Laddering: A Smart Strategy to Maximize Your Savings

One effective way to get higher CD rates while still having periodic access to funds is through CD laddering.

What Is CD Laddering?

Instead of putting all your money into one long-term CD, you split it across multiple CDs with different maturity dates.

Example:

- 6-month CD

- 12-month CD

- 24-month CD

- 36-month CD

As each CD matures, you can withdraw it — or reinvest it into a new long-term CD at a higher rate.

Why CD Laddering Works

- Provides regular access to portions of your money

- Helps you earn higher interest over time

- Reduces interest-rate risk

- Keeps your savings strategy flexible

UIB bankers can help you design the perfect laddering plan for your goals.

Frequently Asked Questions About CDs

1. Can I withdraw money early?

Yes, but there is typically an early withdrawal penalty. CDs work best when you commit to the full term.

2. Are UIB CD rates fixed?

Yes — your rate is locked in when you open the CD.

3. Are CDs safer than stocks?

CDs have been generally considered more reliable. CDs are FDIC insured and never lose value, making them lower-risk.

4. What happens at maturity?

You can withdraw your funds or renew your CD at the current rate.

5. Can I have more than one CD?

Absolutely. Many people hold multiple CDs for goal-based savings or laddering.

Final Thoughts: Why UIB Is the Best Place to Open Your CD

When it comes to building safe, predictable savings, CDs remain one of the best tools available. With competitive rates, local service, and flexible term options, Utah Independent Bank offers CD accounts that fit every stage of life.

Whether you're looking to secure short-term savings or grow your money steadily for years to come, UIB’s CD options provide the security, stability, and value you need to reach your goals.

For more information, visit the UIB CD Rates page or stop by your nearest branch to speak with a local banker.

Start saving smarter today — your future self will thank you.

Disclaimer: The views and opinions expressed in this post do not necessarily reflect the official policy or position of Utah Independent Bank. This post is intended for entertainment and/or informational purposes only and should not be construed as financial advice or an endorsement of any product or service.

This article is for educational and informational purposes only and does not constitute financial advice. Product features, fees, and terms may change and may vary by account type or location. Please refer to the official account disclosures and terms provided by the bank for complete and up-to-date details before making any financial decisions.